The Loyalty Machine

How Starbucks Built the Most Powerful Customer Platform in Retail

A complete analysis of Starbucks Rewards, from gift card to global platform (2001–2026)

Starbucks Rewards is the most sophisticated customer platform in the restaurant industry — a system that collects interest-free deposits, generates $200M+ in annual breakage profit, processes more stored value than 85% of American banks, and drives 60% of U.S. company-operated revenue through 35.6 million active members. No competitor has replicated anything close. But building the infrastructure was the easy part. The harder lesson — one that took a seven-quarter sales decline to learn — is that a loyalty program can only be as strong as the experience it's attached to. When Starbucks lost focus on its stores, no amount of digital sophistication could compensate. Brian Niccol's turnaround, culminating in the strongest quarter in over two years by Q2 2026, is proof that the program was never the problem. It was always the asset. The question was whether the company would build an experience worthy of the loyalty it had earned.

Part I: The Accidental Bank (2001–2015)

A card, not a strategy

The Starbucks Card launched in November 2001 as a simple prepaid gift card — a holiday convenience play, nothing more. Nobody at Starbucks headquarters understood what they had built. The card was a closed-loop, non-redeemable stored value instrument: customers loaded money, spent it on coffee, and whatever remained sat on Starbucks' balance sheet as a liability. Within a decade, customers had loaded $10 billion onto these cards. Today they load $10 billion per year — roughly a quarter of the company's entire revenue flows through prepaid balances before a single latte is poured.

“We're not in the coffee business serving people. We're in the people business serving coffee.”

Howard Schultz, reflecting on Starbucks' early days on the Acquired podcast, described the insight that underpinned everything that followed: "We're not in the coffee business serving people. We're in the people business serving coffee." That philosophy — people first, product second — turned an accidental payment instrument into the foundation of a financial engine that would eventually rival a mid-sized bank.

The financial mechanics are elegant and ruthless. When a customer loads $50 onto a Starbucks card, three things happen simultaneously. First, Starbucks receives cash it can deploy for operations immediately — working capital at zero interest. Second, the customer has psychologically committed to future purchases, converting discretionary spending into sunk cost. As one analysis noted: "By encouraging customers to preload funds, Starbucks eliminates friction at checkout (tap and go), reduces perceived spending (you're not handing over real cash), and boosts frequency (you already 'have money' in your account, so why not use it?)." Third, the credit card processing fee is paid once on the reload, not on every subsequent $5.75 oat milk latte — saving Starbucks millions annually in interchange fees.

Then there is breakage — the quiet profit engine that makes the entire system extraordinary. In 2023, Starbucks recognized approximately $215 million in breakage revenue — funds loaded onto cards that were never redeemed. The breakage rate runs at roughly 10%, and this revenue arrives at near-100% margin. Over the past decade, cumulative breakage exceeds $1.2 billion. To put the growth in perspective: in 2014, breakage revenue was approximately $38 million. By 2023, it had grown to $215 million — a 5x increase during a period when top-line sales merely doubled from $16 billion to $36 billion. Breakage grew faster than the entire company.

As Canadian financial writer JP Koning observed: "Starbucks has around $1.6 billion in stored value card liabilities outstanding. It amounts to roughly 6% of all of the company's liabilities." And the interest rate Starbucks pays on this debt is not zero — it is negative. Koning calculated that when you factor in breakage, "Starbucks already pays 0% on its debts to customers, but add in breakage and that equates to a roughly -10% interest rate." Starbucks doesn't just hold your money for free. It profits from never giving it back.

The stored value flywheel

The stored value system grew at a 16.5% CAGR over twenty years. By 2024, Starbucks held approximately $2.2 billion in outstanding stored value on its balance sheet — a liability that functions as a perpetual, interest-free loan from its own customers. Howard Schultz himself compared this to Warren Buffett's insurance "float" at Berkshire Hathaway: money held before claims are paid, investable in the interim. On the Q2 2022 earnings call, Schultz quantified the scale: "Starbucks customers are increasingly prepaying for their purchases in huge volumes, roughly $11 billion last year, and we are on track to exceed that figure this year. At this moment, well over $1 billion is loaded on Starbucks Cards waiting to be spent in our stores."

The Motley Fool summarized it plainly: "Consumers love Starbucks so much that they're willing to make a deposit to redeem coffee at an unknown future date and time. Starbucks is essentially gaining access to an interest-free line of credit, one that equates to roughly 4% of the company's total liabilities." It is worth noting that 85% of U.S. banks have less than $1 billion in assets. Starbucks, a coffee company, was holding more than twice that in customer deposits.

The system also generated direct investment income. In one fiscal year alone, Starbucks earned approximately $21 million in interest income by investing its float — a line item that does not appear in any competitor's earnings. Starbucks had stumbled into the business of banking without a banking license, without deposit insurance, without regulatory scrutiny, and without the obligation to pay interest. It was, by any financial measure, an extraordinary accident.

The Washington Consumer Protection Coalition eventually accused Starbucks of engineering the system: $5 reload increments and $10 minimums make it structurally difficult to spend down balances to zero, trapping residual funds. The WCPC estimated a $900 million cost to consumers over five years. Starbucks' response was effectively silence. The machine was too profitable to redesign.

Stored Card Value, 2003–2024

Outstanding balance on Starbucks Cards — USD millions

2003, 2023, and 2024 from Starbucks filings. Intermediate years estimated based on 16.5% CAGR.

The rewards layer

Starbucks Rewards launched in April 2008, initially offering modest perks — free Wi-Fi, refillable coffees for frequent visitors. The Gold Card arrived in November 2008 for "super users." By November 2009, these were consolidated into My Starbucks Rewards with three tiers: Welcome, Green, and Gold. The program was visit-based: one star per visit, regardless of spend.

The Starbucks Card Mobile app launched across 9,000+ U.S. locations in 2010. Within a year, 25% of transactions flowed through the card program. The speed of adoption was remarkable, but the strategic implications took years to surface. Starbucks had inadvertently built a closed-loop payment system — a walled garden where the company controlled the entire transaction lifecycle from deposit to purchase to data capture. No bank, no payment processor, no intermediary. As the stored value mechanics noted: "For Starbucks, stored card value is effectively a 'bank deposit'. It's recorded as a liability and Starbucks can use the funds immediately for the business. However, stored value has fewer regulatory requirements than a bank deposit: it can't be redeemed for cash, it doesn't offer interest, and it isn't insured."

To understand why any of this worked, you need to understand the experience it was attached to. Schultz described the early magic on the Acquired podcast: "They would stand up at the coffee bar at the window on Columbia Center. It was at 8–9 o'clock in the morning, they were hanging out there, and then late morning they were coming back. You could just feel the relationship that people were having with one another around human connection. I know it sounds trite, but I could see it back then." The intimacy between barista and customer — names remembered, orders anticipated, small talk exchanged — was the intangible that justified loading money onto a piece of plastic. Schultz called it "the first experiential brand at scale."

Schultz described the organic way the brand's most iconic touchpoint emerged: "That didn't come from me. As the stores got busier and busier, the baristas were having a hard time with whose cup is it? What are we going to do? Someone at Starbucks, I don't know who it was, started writing names on the cup, and it just became standard. So much of Starbucks' success came from customers asking for things we weren't doing, and Starbucks employees who became partners in 1991, understanding the business better than me." The name on the cup — now the most recognizable ritual in global retail — was not a corporate decision. It was a frontline innovation, born from operational necessity and human instinct. It would later become the anchor of the Green Apron Service model that Niccol built his entire store experience around.

The economics of the early model were extraordinary. Schultz recalled: "The economic model and Wall Street, when we went public in 1992, when they heard the model, I said, well, we've never seen a model like that. The model basically was a sales to investment ratio of 2:1 and an operating profit of 20%. You get that two years at the last payback. The retail world had never seen a model like that before." With gross margins approaching 80% on beverages and a two-year payback on new stores, the unit economics gave Starbucks the capital to expand aggressively while funding the Rewards program as a customer acquisition and retention tool rather than a profit center.

At the brand's peak in the Northwest, Schultz noted, "the most loyal customer was coming 18 times a month." That frequency — nearly daily — was the benchmark that the loyalty program would spend the next decade trying to recreate at national scale.

By 2015, the program had reached 10.4 million 90-day active members. The numbers were strong but the structure was wrong. Visit-based earning rewarded the person who bought a $2 drip coffee identically to the person who bought a $7 Frappuccino with three modifications. The economics demanded a redesign. And the redesign would create a flywheel that nobody — not even Starbucks — fully anticipated.

Part II: The Digital Flywheel (2016–2021)

The spend-based pivot

In April 2016, Starbucks made the most consequential structural change in the program's history: shifting from visit-based (1 star per visit) to spend-based (2 stars per dollar). The stated rationale was fairness. The actual rationale was margin optimization — encouraging higher-ticket purchases and premium item exploration. Under the new structure, a $7 Frappuccino earned 14 stars while a $2 drip coffee earned 4. The incentive architecture now aligned with Starbucks' margin structure. Customers were being nudged, gently but systematically, toward the drinks that made Starbucks the most money.

The timing coincided with a broader shift in consumer behavior that Schultz described with characteristic candor: "We didn't have a cold beverage. For the first decade it was zero. To me, there's this thread of at some point shaking off your own opinions and saying, we're going to do what the customer wants us to do." By 2023, cold beverages represented 75% of Starbucks' sales — a complete inversion of the original Italian espresso bar concept. And 60% of beverages were customized, with "extras" on a drink order worth an estimated $1 billion per year in additional revenue, high-margin and easy to push in the mobile app. The spend-based system captured all of this. Every extra pump of vanilla syrup, every non-dairy milk substitution, every topping added through the app earned stars proportional to the price increase. The loyalty program was no longer just tracking visits. It was shaping purchasing behavior in real time.

“The spend-based loyalty program rewarded this behavior, and the data it generated allowed Starbucks to design new drinks”

The shift also revealed a demographic transformation. The customization boom was driven overwhelmingly by younger consumers — Gen Z and millennials — who treated their Starbucks order as self-expression. A Purple Drink with coconut milk and extra ice was not a beverage; it was an identity statement, photographed and posted, a form of social currency. The spend-based loyalty program rewarded this behavior, and the data it generated allowed Starbucks to design new drinks specifically calibrated for customization and social sharing. The product pipeline and the loyalty program were feeding each other in a loop that Johnson would formalize into doctrine.

Kevin Johnson and the Flywheel doctrine

CEO Kevin Johnson, who succeeded Schultz in 2017, built his entire strategic framework around what he called the "Digital Flywheel." The concept was simple but powerful: loyalty drives digital engagement, digital engagement generates data, data enables personalization, personalization increases frequency, frequency drives revenue. Every quarter, Johnson's earnings calls hammered this flywheel with escalating metrics and evangelical conviction.

On the Q4 2017 earnings call, Johnson laid the foundation: "Our priority to accelerate the power and momentum of our digital flywheel reflects the fact that digital relationships are among our most powerful demand generation levers. In fiscal '17, Starbucks Rewards membership in the U.S. rose 11% year over year. Per member spend increased 8% in Q4 alone. The cumulative fact is that today, 36% of tender comes from Starbucks Rewards, the vast majority, via our mobile app."

By Q2 2018, Johnson was widening the aperture: "We are widening the aperture of our Digital Flywheel through a range of customer interaction touch points, including: opening up Mobile Order and Pay to all customers; leveraging Wi-Fi sign-up in our stores; and reinventing Happy Hour through the use of single-use digital coupon, all of which are yielding results."

In April 2019, Starbucks introduced tiered redemption — 25, 50, 150, 200, and 400 stars — replacing the binary "124 stars for a free drink" model. The change gave customers more flexibility but also introduced the psychological architecture that would later enable devaluations. The same quarter, CFO Patrick Grismer quietly noted a favorable accounting change: "We adopted the new revenue recognition accounting standard this fiscal year and for the most part, the standard reclassifies stored value card breakage from the interest and other line below operating income and outside of segment results to the revenue line at the segment level." Translation: breakage revenue, previously buried below operating income, was now flowing directly into top-line revenue and segment margins — a 40-basis-point tailwind that made the Americas segment look even more profitable.

The Digital Flywheel

Kevin Johnson's loyalty framework, articulated on the Q4 2017 earnings call

Framework articulated by CEO Kevin Johnson on the Q4 2017 earnings call.

Deep Brew and the AI layer

Johnson also introduced "Deep Brew" — Starbucks' internal AI platform for personalized marketing, labor optimization, and inventory management. On the Q4 2019 earnings call, Johnson described it in characteristically grand terms: "Over this past year, we have been dialing up our in-house capabilities and investments in AI with an initiative we call Deep Brew. Deep Brew will increasingly power our personalization engine, optimize store labor allocations and drive inventory management in our stores. We plan to leverage Deep Brew in ways that free up our partners so that they can spend more time connecting with customers."

By Q4 2021, Deep Brew had expanded into pricing: "We're actually using machine learning and some of the Deep Brew technologies that inform our pricing team on where and how to take that price." The platform powered the push notifications and personalized offers that drove incremental visits — but also contributed to the discounting culture that would later become a liability. When an AI engine is optimized for engagement, it discovers that the fastest path to engagement is often a coupon. Deep Brew was doing exactly what it was designed to do. The problem was that nobody questioned whether the objective function was correct.

Even Narasimhan, years later, would lean on Deep Brew for exactly this purpose. On the Q1 2024 earnings call, he described: "We activated new capabilities within our proprietary Deep Brew data analytics and AI tool to identify and incentivize specific rewards members cohorts." The language revealed the approach — "identify and incentivize" meant finding customers at risk of churning and offering them discounts to stay. AI-powered retention through coupon distribution. The flywheel was spinning, but it was spinning in the wrong direction: each discount trained customers to expect the next one.

Stars for Everyone: the growth-versus-profit trade-off

The true inflection point came in September 2020 — mid-pandemic — when Starbucks launched "Stars for Everyone," removing the requirement that customers pay with a pre-loaded Starbucks card to earn stars. Any payment method now earned rewards. This was a massive strategic bet: Starbucks sacrificed the stored value reload incentive (and its associated financial benefits) in exchange for sheer membership growth.

On the Q4 2020 call, Johnson was measured but optimistic: "The successful launch of Stars for Everyone in mid-September was a key highlight in the quarter. These early results indicate that the flexibility of rewards payment options, including the removal of the stored value card requirement to earn stars, is resonating with customers. This gives us optimism regarding our ability to meaningfully grow the number of 90-day active Starbucks Rewards members in fiscal 2021."

+28%

active members in one year

Brady Brewer, then CMO, explained the philosophy: "We've looked at things like Stars for Everyone, trying to lower the barriers to entry so that customers can get the benefits of the program and experience the incentives and the personalized experience they get through the program. Lowering those barriers to entry, reaching as many people with the program, and then ensuring that the incentives and the services attached to that program make the experience personalized and effortless."

The bet paid off spectacularly in raw numbers. Active members surged from 19.3 million to 24.8 million in a single fiscal year — a 28% increase. On the Q4 2021 call, Johnson trumpeted the milestone: "We grew our 90-day active Starbucks Rewards members representing our most loyal and engaged customers by approximately 30% in fiscal year '21 to 24.8 million members. Noteworthy is that in Q4, 51% of U.S. tender for company-operated stores was generated by this loyal customer base."

But the trade-off was real and structural. Every member who earned stars on a credit card instead of a pre-loaded card represented lost float, lost breakage, and higher interchange fees. The financial engine that made Starbucks Rewards uniquely profitable was being diluted by the growth engine that made it uniquely large. The question of whether growth or profitability should govern the program's design would haunt the next four years.

The tokenization tease

On the Q4 2021 earnings call, Johnson dropped a line that briefly electrified Web3 observers: "Through blockchain or other innovative technologies, we are exploring how to tokenize Stars and create the ability for other merchants to connect their rewards program to Starbucks Rewards. This will enable customers to exchange value across brands, engage in more personalized experiences, enhance digital services and exchange other loyalty points for Stars at Starbucks."

The ambition was staggering. Johnson was describing Stars as a portable digital currency — appreciating in value through network effects, exchangeable across brands, sitting on modern payment rails. He continued: "Over the next year, you will see the first instance of this loyalty points exchange with other consumer brands. This approach will also serve as a foundation for a more aspirational concept for new, modern payment rails that align payment expenses with the value received by customers and merchants."

2PM's "StarDAO" member brief argued Starbucks was the perfect candidate for a decentralized autonomous organization to govern its loyalty program. Consumer investor Magdalena Kala captured the vision: "Imagine earning Starbucks tokens as an early customer in Seattle and seeing their value appreciate over time as the brand expands nationally and internationally. Or imagine getting actual equity allocation pre-IPO due to high token ownership." The brief's thesis: "Before, loyalty was paid in discounts. In the future, it may be paid with appreciation."

It never happened in that form. But the intellectual foundation — loyalty as ownership, not just transaction — would inform what came next.

Part III: The NFT Detour and Identity Crisis (2022–2024)

Schultz returns

Howard Schultz returned as interim CEO in March 2022 — his third stint running the company. The scale of what he was returning to manage was staggering. On the Q2 2022 earnings call, Schultz quantified the digital business he had helped create: "Mobile Order & Pay, an over $4 billion business, is up 400% in five years, is up 20% over last year. Our $500 million delivery business is up 30% over last year. The Starbucks Card puts our brand in the hands of nearly 120 million people and is alone larger than the entire gift card category." Mobile Order & Pay had gone from a convenience feature to a $4 billion revenue channel in five years. And yet, as Schultz would soon discover, the speed of that growth had outrun the company's ability to deliver the experience that justified it.

The digital third place

On the same call, he framed the opportunity in Web3 with characteristic sweep: "I believe Web 3.0 will create an authentic digital third place experience and drive substantial new revenue streams for Starbucks and be accretive to the brand." CMO Brady Brewer elaborated with a vision that was genuinely compelling:

“I believe Web 3.0 will create an authentic digital third place experience”

Brewer continued: "Emerging technologies associated with Web 3, and specifically NFTs, now enable this aspiration. We are creating the digital third place. To achieve this, we will broaden our framework of what it means for people to be a member of the Starbucks community, adding new concepts such as ownership and community-based membership models that we see developing in the Web 3 space." He painted a picture: "Imagine acquiring a new digital collectible from Starbucks, where that product also serves as your access pass to a global Starbucks community, one with engaging content experiences and collaboration all centered around coffee."

Starbucks Odyssey launched in December 2022 as a loyalty extension built on the Polygon blockchain. The design was deliberately un-crypto: NFTs were called "Journey Stamps," purchasable with credit cards, no wallet required. As Brewer told TechCrunch: "It happens to be built on blockchain and web3 technologies, but the customer — to be honest — may very well not even know that what they're doing is interacting with blockchain technology. It's just the enabler."

Ownership changes experience

Adam Brotman — the architect of Mobile Order & Pay a decade earlier — was brought in as advisor through his company Forum3. His framing captured the ambition better than anyone: "Get out of the linear spend and earn and get into more participate to collect and win." In a Fast Company interview, Brotman expanded on the intellectual framework: "Loyalty programs today tend to be pretty linear: You spend money to get points and convert those points into coupons or discounts. For a brand that wants to think about ways that aren't so discount heavy and that can be more participatory and about storytelling and loyalty, this is an exciting place to explore. It's about a customer strategy, not a web3 strategy."

Brotman saw something that most critics missed. Digital collectibles, he argued, were not speculative assets — they were a new form of brand relationship: "Coming from my background at Starbucks and then J.Crew, I was just fascinated by the idea of a digital asset that anybody — let alone a brand — could manufacture or create that was both a collectible but also digital media and programmable. That hybrid of those things was so interesting to me because, for the most part, brands have to choose between creating a product or giving a discount or just using digital media in some ways. The ability to put these things together, it changes the experience. Ownership changes experience. It creates these new network effects."

The program offered "Journeys" — interactive challenges that educated members about coffee and earned them NFT stamps. Rewards included virtual espresso martini-making classes, trips to Starbucks' Costa Rica coffee farm, and limited-edition stamps tradeable on OpenSea. The collecting psychology was deliberate: Starbucks' physical "Been There Series" ceramic mugs already demonstrated that their customers were natural collectors, with some complete sets selling for thousands on eBay.

The intellectual framework was sound. The timing was catastrophic.

The experience falls apart

While Starbucks invested executive attention in blockchain, the core business was deteriorating. Mobile Order & Pay had crossed 31% of U.S. transactions by mid-2024, and the operational consequences were severe. Schultz described the breaking point on the Acquired podcast with vivid specificity: "The thing I remember the most is that we were in Chicago at 8:00 AM because people wanted to show me the problem. Everyone is getting off the loop, the train at 8:00 AM, and everyone who ordered on their app says the same thing, your drink's going to be ready in seven minutes. Everyone shows up, and all of a sudden we got a mosh pit, and that's not Starbucks."

The mobile app — once Starbucks' greatest innovation — had become what Schultz called "the biggest Achilles heel for Starbucks. And it's not even a close second." He elaborated: "The mobile app created unbelievable convenience for our customers. But remember, we are an experiential brand. As this thing was growing, there was never an opportunity because it became so seductive for the company. All that is true, but it was beginning to deteriorate at a rapid rate, the third place experience in the sense of community."

Schultz was unflinching about what had gone wrong: "The company did not do a good job of anticipating the technological refinements that needed to be put in place to avoid what was happening." And: "The stock was at record high, the company was not investing ahead of the curve, not paying attention to the velocity of the mobile app and what it was becoming until it was too late."

By Q2 2024, Narasimhan's team was quantifying the damage on the earnings call: "More than 60% of our morning business in the U.S. comes from Starbucks Rewards members who overwhelmingly order with a Starbucks app. What's interesting though, despite strong Mobile Order & Pay sales, we saw a mid-teens percent order incompletion rate within the order channel this past quarter." A "mid-teens percent" incompletion rate meant that roughly one in seven mobile orders was going uncompleted — customers abandoning pickups due to long wait times. The app that was supposed to reduce friction was creating new friction at scale.

The Narasimhan interregnum

Laxman Narasimhan became CEO in March 2023. His tenure — barely 18 months — was defined by a brutal deterioration in the core business. Comparable store sales turned negative for the first time in years, reaching -7% in China and -2% in the U.S. by Q4 2024.

The loyalty program, meanwhile, had become exactly what critics feared: a coupon book. Starbucks was spending aggressively on discounted transactions to prop up comparable store sales. Narasimhan described the approach on the Q1 2024 call: "We activated new capabilities within our proprietary Deep Brew data analytics and AI tool to identify and incentivize specific rewards members cohorts." Translation: the AI was finding customers who might churn and throwing coupons at them. The program that was supposed to build frequency was instead subsidizing transactions that would have happened anyway. Rewards members were being trained to wait for deals rather than visit habitually.

Even the membership growth that Narasimhan trumpeted was masking the problem. On the Q3 2023 call, he announced: "Active Starbucks Rewards membership in the U.S. exiting Q1 totaled over 30 million members, up 4 million members or 15% over last year. Loyal Starbucks Reward members drove a record 56% of tender." The numbers were growing. But per-member economics were degrading. More members, spending on discounted transactions, generating less profit per visit.

“confirming a bitter truth about loyalty programs: once locked in, they absorb punishment rather than leave.”

In February 2023, Starbucks implemented a major devaluation: star requirements increased 33–100% across redemption tiers. A brewed coffee went from 50 to 100 stars. The popular 50-star tier was eliminated entirely. The backlash was fierce — but membership still grew 15% that year, confirming a bitter truth about loyalty programs: once customers are locked in, they absorb punishment rather than leave. The stored value on their cards makes switching psychologically expensive, even when the math says they should.

The diagnosis

Howard Schultz, watching from the board, posted a public critique on LinkedIn in May 2024 that read as a thinly veiled indictment. His prescription was precise: "The stores require a maniacal focus on the customer experience, through the eyes of a merchant. The answer does not lie in data, but in the stores." And: "One of their first actions should be to reinvent the mobile ordering and payment platform — which Starbucks pioneered — to once again make it the uplifting experience it was designed to be." His framing captured the core tension: "Through it all, focus on being experiential, not transactional."

The hundreds of comments on Schultz's post painted a consistent picture of what had gone wrong at the store level. A current barista described a systemic shift: "A major shift from an experience-focused company to a production-focused one. The new Starbucks is all about production now, especially sugar-based drinks, targeting younger clientele with very much less focus on the high quality hand-crafted coffees. Today, Starbucks is more about producing more and as fast as possible to the maximum customer count possible with the least number of partners on the floor."

A loyal customer described the experience degradation: "A 5-minute 'buy a hot drink' experience has become a 20-minute 'watch the colorful sugar drinks go by' experience." Another described the mobile-first store redesigns: "Starbucks revamped 3 stores in my area to mobile-first. It cut seating in the stores to almost nothing, pushing out long-time customers who go there to work and meet. There is a 4th store that is now 100% mobile only and you can't even order anything from the register. When I tried the location out, half the people coming in were older people who didn't understand and then left mad."

A pricing critique cut to the core: "Why would a consumer buy a $4-7 coffee at Starbucks when they can go to a craft coffee shop and get higher-quality coffee for the same price? Starbucks is a chain, you cannot compete on artisan products with a craft coffee shop." A retired partner described the human cost: "Store leaders create the environment and their partner experience is abysmal at best. They are overworked, underpaid, and ignored, and it has turned into the classic burn-and-turn retail approach."

The structural bind

On the Acquired podcast, Schultz framed the structural bind with a phrase that captured the paradox: "Ubiquity is an enemy of Starbucks. We have to be defined by the one store you come into, not based on the thousands." He elaborated: "The worst thing that Starbucks could have become, and the worst thing that Starbucks could become is a utility. Scale and ubiquity creates complexity. Complexity demands efficiency. But we are in a business where that touch point between the customer and the barista has to be protected and has to be elevated."

The paradox was clear to anyone paying attention. The app was too lucrative to retreat from — stored value, breakage, data, reduced credit card fees — but it was systematically destroying the "Third Place" premium that justified Starbucks charging $6 for a drink available at a thousand competitors. Stores designed for mobile-first operations had cut seating and eliminated the behaviors — lingering, socializing, working — that justified the premium pricing. Starbucks had optimized for throughput and displaced its own identity. Independent coffee shops, with their leather chairs and handwritten menus, were capturing the old Starbucks vibe. Starbucks had disrupted itself out of its own soul.

On the Q1 2023 earnings call, Odyssey received a brief mention. By Q3 2023, it vanished from the earnings narrative entirely. It was never mentioned again. The NFT market had collapsed. Crypto sentiment had turned toxic. More fundamentally, Odyssey solved a problem that most Starbucks customers did not have. The 34 million Rewards members wanted faster drinks and shorter lines, not digital collectibles.

Part IV: The Subtraction (September 2024–Present)

Niccol arrives

Brian Niccol became Starbucks CEO in September 2024 with a mandate as clear as any in corporate history: fix it. His credentials were specific and relevant. At Chipotle, he had inherited a brand buried under food safety scandals and a digital strategy that barely existed. He doubled revenue from $4.8 billion to $9.9 billion in five years. Profit grew nearly sevenfold. The stock rose 773%.

“Launch a loyalty program that is deliberately, almost aggressively, simple:”

The Chipotle playbook was deceptively simple. Fix food safety protocols. Build a second make-line — called "Chipotlanes" — for digital orders so mobile customers stop clogging the in-store experience. Launch a loyalty program that is deliberately, almost aggressively, simple: spend $125, get a free entrée. No tiers, no confusion, no gaming. The program hit five million members in four months and reached 20 million. Throughput became the obsessive metric — the Boston Financial District store went from mid-20 entrées in a peak 15-minute window to 40+.

The Chipotle insight that Niccol brought to Starbucks: customers don't leave because the menu is stale. They leave because the experience is broken. And the fastest path to fixing an experience is not to add something new. It is to remove what broke it.

On the Q4 2024 earnings call — his first — Niccol was direct about the diagnosis: "Our financial results were very disappointing, and it is clear we need to fundamentally change our strategy to win back customers and return to growth. Back to Starbucks is that fundamental change. We have to get back to what has always set Starbucks apart, a welcoming coffee house where people gather and where we serve the finest coffee, handcrafted by our skilled baristas." He identified the loyalty program's distortion with precision: "I've heard that while people love Starbucks, some feel like we have drifted from our core. We've made it harder to be a customer than it should be, and we focused our marketing too narrowly on Starbucks Rewards members."

"Back to Starbucks": three subtractions

Niccol's strategy — branded "Back to Starbucks" — had three moves. Each one was a subtraction.

First, strip the menu. Fewer modifications, fewer limited-time offers. The goal was to reduce barista cognitive load and shorten fulfillment time. He introduced the "SmartQ" algorithm to optimize order sequencing. By Q2 2026, 80% of stores were hitting the four-minute target for both café and drive-thru orders. Schultz had diagnosed the problem on the Acquired podcast: "Ten thousand little scratches of efficiency that dilute the experience." Niccol's approach was the inverse — reduce complexity to restore quality.

Second, rebuild the store as a place, not a vending machine. Niccol committed $500 million to refresh 1,000 locations by end of 2026 — warm materials, local design elements, and actual seating. He introduced the "Green Apron Service" model, structured around five scripted customer moments: the greeting, the order, the handcraft, the handoff with the customer's name, and the farewell.

The physical redesign was deliberate in its symbolism. Dawn Clark, SVP of Global Concepts and Design, described the philosophy behind the two most tangible artifacts of the refresh — a new ceramic cup and a new plush green chair: "They are the biggest signals we have of warmth, comfort, and generosity." The new ceramic cups — five glazed options in white and green, sharing a tapered silhouette inspired by Italian espresso culture — would be offered to customers who stay to enjoy their coffee. The new chair — green velvet, wood-framed — was a deliberate revival of the iconic 1990s oversized purple velvet armchair that defined the original Third Place aesthetic. Clark recalled the inspiration: "What was great about that chair is it was oversized; it wasn't practical. It was very much like you could maybe have two people sit in it, you could put your feet up, swing your legs over the arm. That was a big part of the inspiration — and also the lushness of the texture."

Clark was candid about the design philosophy: "It's a little overly generous in its invitation to be comfortable. Part of what we're in a way saying, it doesn't exist to be convenient or easy to maintain. It exists to provide comfort. And we're willing to take on the challenge." Niccol's stated ambition for the chair was characteristically specific: "It's got to be the seat that when you walk in, you're like, 'Man, I can't wait for him to get up. I'm hopping in that chair the second he does.'" The logic is unit economics, not nostalgia. Customers who sit down order more.

Third, and most consequentially, rewire loyalty from discounts to frequency. This is where Niccol's diagnosis was sharpest. The Rewards program under Narasimhan had become a deal-distribution machine. Starbucks was training its best customers to be price-sensitive — the opposite of what a premium brand should do.

“We started by reducing the frequency of discount-driven offers”

On the Q1 2025 earnings call, Niccol quantified the shift: "We started by reducing the frequency of discount-driven offers, resulting in 40% fewer discounted transactions year over year." The results were counterintuitive and revealing: "Non-Starbucks Rewards customer traffic grew quarter over quarter. Starbucks Rewards membership and spend grew both quarter over quarter and year over year." Fewer discounts did not mean fewer customers. It meant higher-quality transactions.

By Q2 2025, Niccol articulated the philosophy explicitly: "Our goal is that every transaction is higher quality and more profitable. We are driving more durable growth by moving away from highly discounted offers, building the foundation of a healthier base business to grow from."

On the Q4 2025 call — marking one full year of the turnaround — Niccol reported: "Non-Starbucks Rewards customer transactions grew year over year for the second consecutive quarter across all dayparts, validating our approach to marketing. And value perception strengthened across all generations in the fourth quarter and for the fiscal year, driven by our investment in Green Apron service, and our proactive moves to bring back the condiment bar, simplify our pricing architecture, and remove the extra charge for nondairy milks."

The March 2026 relaunch

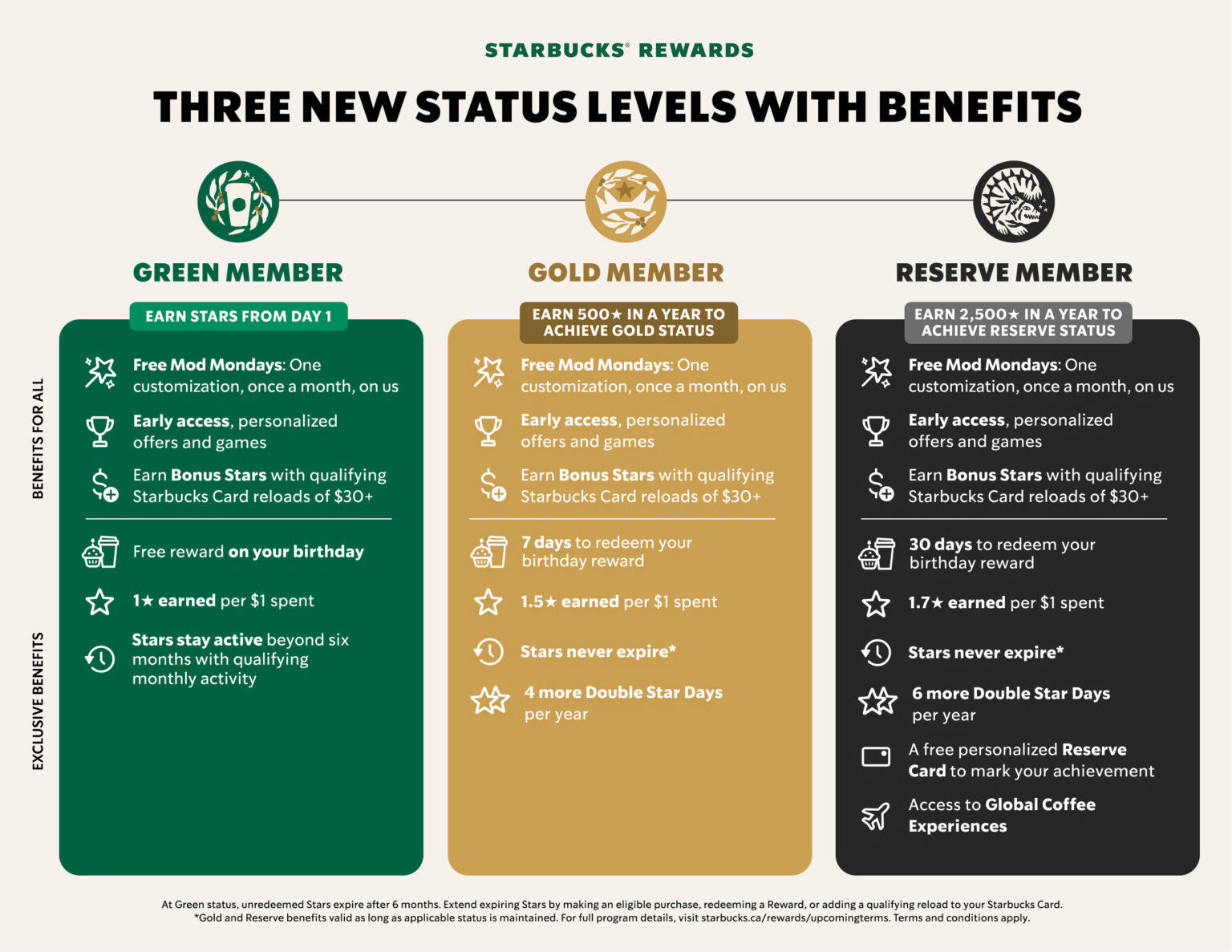

On March 10, 2026, Starbucks launched a completely reimagined Rewards program with three tiers — Green, Gold, and Reserve — each offering escalating earning power and benefits. This was not a tweak. It was a structural redesign built on a specific behavioral insight: the old program rewarded saving, the new program rewards spending.

The mechanics: Green members earn 1 star per dollar. Gold members earn 1.2 stars. Reserve members earn 1.7 stars. Redemption tiers were restructured with dollar caps — $2 off at 60 stars, $6 at 100 stars, $10 at 200 stars, $16 at 300 stars — to control the cost of excessive modifications that had been gaming the old system. Stars no longer expire at Gold and above.

The strategic centerpiece was the new 60-star redemption tier: $2 off any item. It was introduced directly in response to member feedback asking for quicker access to rewards. Within weeks, it became the most popular redemption option, accounting for more than a quarter of all redemptions. The first Free Mod Monday — a complimentary drink modification for members on one Monday per month — more than doubled point redemptions compared to the prior promotional format.

The design logic is precise and reveals Niccol's understanding of behavioral psychology. A low-barrier, high-frequency redemption drives visit cadence rather than saving behavior. The old 150-star free drink rewarded patience and deferred gratification — visit less often, accumulate more, get a big payoff. The 60-star tier rewards immediacy — visit frequently, redeem quickly, come back tomorrow. It is cheaper for Starbucks than the old free-drink rewards, but it is used far more often, creating a compounding visit loop.

The reload bonuses — 10 bonus stars for a $30+ reload, 25 for $50+ — quietly rebuild the stored value flywheel that "Stars for Everyone" had diluted. Members capitalizing on easy ways to earn more stars are loading funds onto their cards — funding Starbucks' balance sheet in advance of the visit. The stored value float that was structurally weakened in 2020 is being rebuilt by 2026, not through coercion but through incentive design.

The backlash was predictable and absorbed. A TikTok video criticizing the changes racked up over half a million views within 24 hours. Long-time Gold members were furious about being reset to Green. Green-tier members paying with pre-loaded cards saw their earning rate effectively halved — from 2 stars per dollar to 1 star per dollar. But the program was designed to reward frequency, not tenure. The tiers create aspiration. The 60-star tier creates habit. The combination creates a flywheel that compounds visits rather than discounts.

The Coffee Loop experiment

One smaller experiment is worth noting for what it reveals about Niccol's iterative approach. In October 2025, Starbucks quietly piloted "Coffee Loop" — a standalone punch-card program for non-Rewards customers. The idea: capture the casual customer segment that refuses to download apps or create accounts, using the simplest possible loyalty mechanic (buy X, get one free). The pilot ran in select markets for six months before ending on April 30, 2026, citing data-silo challenges — the punch-card transactions couldn't feed back into Starbucks' personalization engine. The lesson confirmed Niccol's broader conviction: simplicity matters, but so does data integration. Loyalty without data is just generosity.

The results

By Q2 2026 — the quarter ending March 29, 2026 — the turnaround was unmistakable.

Revenue rose 9% year-over-year to $9.53 billion. North America comparable store sales increased 7.1%, driven by 4.4% transaction growth and 2.6% average ticket increase. Global comparable store sales rose 6.2%. It was the strongest quarter in over two years and the first to deliver combined top-and-bottom-line growth since 2023.

The loyalty metrics were equally striking. On the Q2 2026 earnings call, Niccol reported: "U.S. 90-day active Starbucks Rewards membership reached a record 35.6 million with both rewards member and nonmember transactions growing year-over-year. Our new 60-star redemption option has become our most used reward, accounting for approximately 1/3 of all redemptions. And while still early, we've seen a growing number of customers visit 4 or more times a week since launching last month. We've made Starbucks Rewards a growth engine again, positioning it to drive new customer routines, deeper engagement and increased frequency."

60%

of U.S. revenue is from members

Rewards members generated approximately 60% of U.S. company-operated revenue — roughly $13 billion annually — while spending 3x more per person and visiting 5.6x more frequently than non-members. Nearly half (48%) of all mobile users who regularly use restaurant apps use Starbucks Rewards — the single largest user base in the industry. Customer retention stood at approximately 44%, versus an industry average of 25%.

Starbucks raised full-year 2026 guidance: comparable store sales growth of at least 5% (up from 3%), and adjusted EPS of $2.25–$2.45 (up from $2.15–$2.40).

Part V: What the Arc Reveals

The three-layer architecture

Twenty-five years of iteration produced something that transcends any individual program redesign: a loyalty platform that is, at its foundation, three businesses stacked on top of each other.

Layer 1: A bank. $2.2 billion in stored value, $200M+ in annual breakage, zero-cost float, reduced interchange fees, and approximately $21 million in annual investment income. This layer is invisible to customers and nearly impossible to explain in marketing copy. But it is the foundation — the financial engine that makes Starbucks Rewards profitable at a structural level before a single star is earned or redeemed. As the 2PM brief noted: "Starbucks began as a coffee roaster, but today it's just as much of a financial services company."

Layer 2: A data engine. 35.6 million identified customers generating transaction-level behavioral data that powers Deep Brew's personalization, labor scheduling, inventory management, and marketing. With 71% of app users visiting at least once a week, and members visiting 5.6x more frequently than non-members, the dataset is unmatched in the restaurant industry. This is the competitive moat — the accumulation of a decade of behavioral signal that no competitor can buy or build quickly.

Layer 3: A behavior system. Stars, tiers, streaks, challenges, Free Mod Mondays, and the social signaling that shapes when, how often, and how much customers spend. This is the most visible layer and the most discussed. It is also the most prone to mismanagement — the layer that became a coupon distribution machine under Narasimhan and that Niccol rebuilt around frequency rather than discounts.

The architecture explains why no competitor has come close. Dutch Bros has perhaps the strongest loyalty penetration in the industry: 72% of transactions flow through Dutch Rewards. But Dutch Bros has no stored value float, no closed-loop payment system, and roughly 1,000 locations versus Starbucks' 17,000+ U.S. company-operated stores. It has layer 3 without layers 1 or 2. McDonald's MyMcDonald's Rewards spans 50+ markets with approximately 210 million global members — a scale that dwarfs Starbucks. But McDonald's operates primarily through franchisees, meaning it lacks direct ownership of the customer relationship. There is no stored value float, no breakage revenue, and limited personalization depth. Panera's Unlimited Sip Club demonstrated an alternative model — subscription-driven frequency — but subscriptions create brittle retention: when a customer cancels, the relationship ends. Starbucks' stored value model does the opposite: money already loaded on the card pulls customers back even during periods of reduced enthusiasm. Independent coffee shops have, ironically, become the most credible competitors to Starbucks' original value proposition — but they cannot build a data engine at scale. The competitive advantage of community does not compound the way the competitive advantage of data does.

Starbucks' loyalty retention rate of 44% versus an industry average of 25% is the output of all three layers operating in combination. The bank funds the program. The data engine personalizes it. The behavior system drives the habits. Remove any layer and the math deteriorates. No competitor has all three.

Three-Layer Platform Architecture

Stacked advantages no competitor has replicated in full

Layers 1 and 2 are permanent, compounding advantages. Layer 3 is a mirror — it reflects whatever quality the underlying experience delivers.

The unreplicable machine — and its one dependency

Layers 1 and 2 are self-reinforcing and highly durable. Stored value float grows as membership grows. Data quality compounds as behavioral history deepens. These advantages require not just capital but time — years of transaction data from tens of millions of identified customers, layered onto a closed-loop payment system that no competitor stumbled into building the way Starbucks did in 2001.

Layer 3 is the fragile one. It is the layer customers actually experience, and it is the layer most directly coupled to the quality of the in-store visit. When the stores deteriorated — when wait times hit 20 minutes, when the menu became an engineering challenge, when the mobile app turned the lobby into a mosh pit — layer 3 began optimizing for the wrong objective. Coupon distribution masquerading as personalization. The behavior system was compounding a problem, not solving one.

This is the structural insight the arc makes visible: layers 1 and 2 are permanent advantages. Layer 3 is a mirror — it reflects back whatever quality the underlying experience delivers. When the experience is strong, the behavior system builds habits. When the experience is broken, it builds deal-seekers.

The experience imperative

Schultz captured this on the Acquired podcast with a phrase that should be read by every loyalty program manager in the world: "We're not in the transaction business. We have to execute transactions, but that has to go through the lens of being an experience business, an experience place. People are longing for human connection."

The Starbucks loyalty story is, at its deepest level, a story about what it costs to forget that. The program generated $200M in annual breakage and held $2.2 billion in stored value while the core experience was deteriorating. The financial metrics stayed healthy long after the experiential ones had turned. That lag — between when the stores went wrong and when the numbers caught up — is what made the crisis so hard to diagnose in real time. The machine kept running on its own momentum.

Niccol's turnaround was not a program redesign. It was an experience redesign that made the program relevant again. Forty percent fewer discounted transactions. A 60-star redemption tier that rewards daily visits rather than patient accumulation. A new store model built for connection — green velvet chairs, ceramic cups, a barista who writes your name. The program didn't change fundamentally; the experience around it did. And the program responded: record membership, 4.4% transaction growth, the strongest quarter in over two years.

The ceramic cups, the green velvet chairs, the 60 stars for $2 off — these are not innovations. They are restorations. The platform was always sound. What it needed was an experience worthy of the loyalty it had already earned.

Twenty-five years and 35.6 million members later, the conduit is still flowing.

Mathias Coudert